The Continent Snapshot

Africa opens 2026 on a bull run

While global indices struggled under the weight of rising Middle East tensions and oil price spikes in late March, the S&P 500 fell roughly 1.7% in the final week of the quarter. African stock markets were busy setting all-time highs, cutting interest rates, and watching their

currencies strengthen. The continent did not move as one, but the direction was unmistakably positive.

Fifteen African central banks held monetary policy meetings in the first two months of the year. Eight of them cut rates, including Kenya,

Egypt, Angola, Ghana, Mozambique, Zambia, Nigeria, and the Democratic Republic of Congo. This easing wave signals something

important: after more than two years of aggressive rate hikes to fight post-pandemic inflation, African policymakers now have enough

confidence to start putting growth back on the agenda. Inflation has cooled in several countries, including Kenya, Zimbabwe, Ghana, and

Zambia. That change in direction matters for investors.

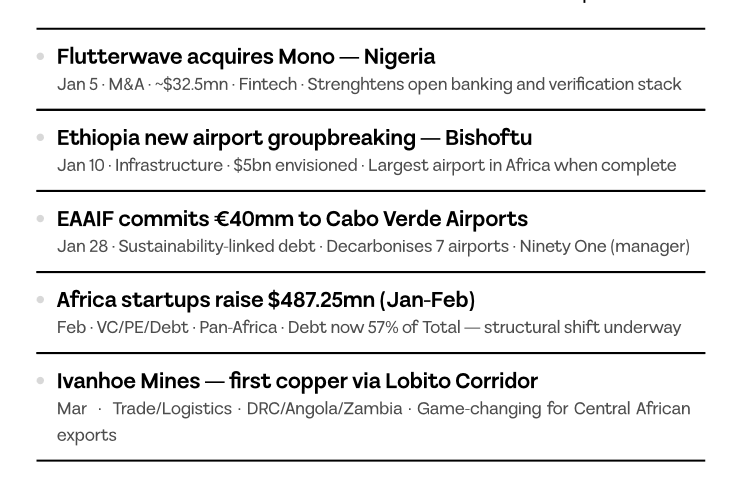

At the same time, African startup ecosystems raised $487.25 million in the first two months of 2026, an 11% increase over the same period in 2025. The composition of that money is shifting, though. Equity capital fell significantly, while debt financing more than doubled. Investors are becoming more selective and more structured. The era of easy venture money may be fading, but the demand for African solutions is not.