Introduction

Africa stands at an essential moment in its economic transformation, with the world’s fastest-growing population and vast natural resources. The continent possesses the foundational resources required for sustained and inclusive growth. Yet, rooted structural challenges such as limited access to finance, infrastructure deficits, volatile commodity markets, and youth unemployment continue to hinder the full realization of this potential. The Africa Grow framework positions the continent’s development around interconnected economic pillars that address both immediate needs and long-term opportunities. By strengthening agriculture, expanding financial inclusion, accelerating digital innovation, promoting sustainable investment principles, unlocking infrastructure, and elevating job-creating industries, Africa can create a pathway toward resilience, progression, competitiveness, and shared prosperity.

You might ask, why does this report matter? Africa is entering a period of heightened economic urgency. Population growth, climate stress, global capital reallocation, and geopolitical fragmentation are converging at a time when the continent must create jobs, raise productivity, and stabilize living standards at unprecedented scale. Despite abundant potential, growth outcomes across Africa remain uneven, volatile, and insufficiently transformative. This report matters because it moves beyond fragmented sectoral analysis and presents an integrated, evidence-based assessment of Africa’s growth engines and constraints. It identifies not only where growth is occurring, but why it is failing to translate into food security, jobs, energy access, and inclusive prosperity. By grounding the analysis in data across six foundational pillars, the report provides clarity in a complex policy and investment environment. In a context where decisions are increasingly shaped by environmental, social, and government criteria, fiscal constraints, and domestic capacity limits, the pace of development across Africa is. Africa Grow offers a structured lens to prioritize reforms, allocate capital more effectively, and align public and private actions.

Context

The Africa Grow report serves three core functions. It diagnoses Africa’s growth system by assessing the performance and interdependence of six critical pillars: agriculture, banking and capital, environment, social, and governance (ESG), fintech, jobs and trade, and power, energy, and infrastructure using regional and country-level data. This systemic approach reveals where bottlenecks in one pillar undermine progress in others. By translating data into strategic insight rather than presenting data in isolation, the report links quantitative indicators to policy outcomes, investment behaviour, and institutional capacity. It highlights structural accelerators, binding constraints, and cross-sector feedback loops that shape growth trajectories. Also, bridging policy and investment perspectives is relevant to policymakers, investors, development partners, and private-sector leaders. It frames growth challenges in terms of risk, return, resilience, and inclusion.

The Africa Grow report has five primary objectives:

(1) To provide a coherent growth framework by establishing a unified analytical framework that explains Africa’s growth dynamics across interconnected sectors.

(2) To support better decision-making by equipping governments, investors, and development institutions with actionable insights to prioritize reforms, deploy capital, and design interventions with the highest systemic impact.

(3) To identify scalable growth pathways by highlighting policies, technologies, and institutional models that have demonstrated results and can be replicated or scaled across countries and regions.

(4) To align growth with inclusion and sustainability – integrate environment, social, and governance, job creation, and climate resilience into the growth narrative, ensuring that economic expansion translates into social and environmental gains. (5) To shift the narrative from potential to performance by moving the Africa growth discussion from aspirational promise to measurable outcomes, execution capability, possibility, and accountability.

Background

Africa’s economic trajectory is at an essential juncture. Over the past two decades, the continent has recorded periods of strong growth, rising investment interest, and meaningful progress in financial inclusion and infrastructure development. Yet these gains have been uneven, frequently disrupted by external shocks, and insufficient to deliver sustained improvements in productivity, job creation, and living standards at the scale required by Africa’s rapidly expanding population. Africa is home to the world’s youngest and fastest-growing population, with millions of new candidates joining the labour market each year. At the same time, the continent faces persistent structural challenges, including low agricultural productivity, infrastructure and energy deficits, shallow financial systems, climate vulnerability, and high levels of familiarity in employment. These constraints have limited the capacity of economic growth to translate into broad-based development outcomes.

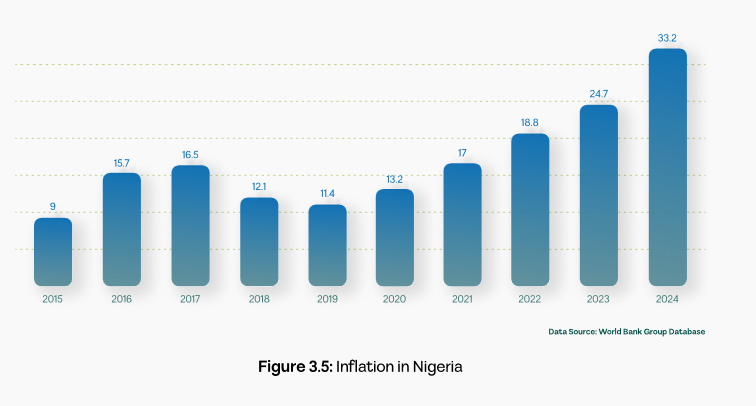

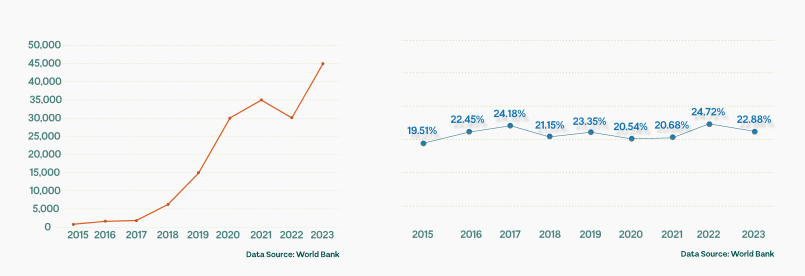

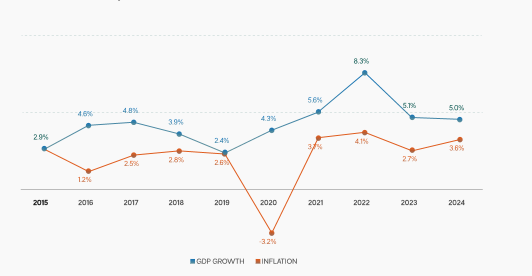

Figure 1 shows the growth rate of Sub-Saharan Africa. GDP suffered a negative growth rate in 2020 across the entire region due to the pandemic lockdown (no export/import). GDP has a 17% growth rate from 2015 to 2024, from $1.69 trillion to $1.98 trillion, respectively, despite the fluctuations. There has been a gradual rise in inflation during the same time frame, due to factors such as the exchange rate, consumer price index, demand, and supply pushed inflation. Inflation has an increment of 72% from 2015 to 2024; this significant increase affected the standard of living and also affected businesses.

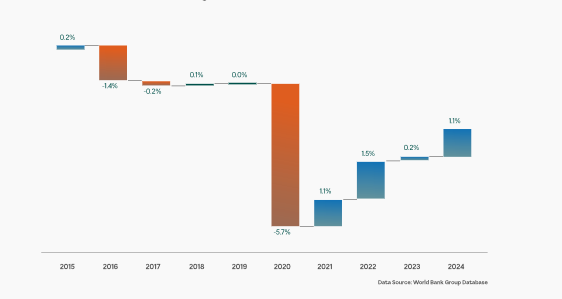

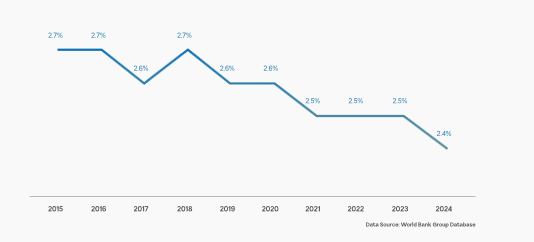

Figure 2 has positive growth rate per capita in 2015, 2018, 2021, 2022, 2023, and 2024. Which means the economy grew faster than the population, or the population growth is slow or declining. The population growth rate actually declined from 2.7% in 2015 to 2.4% in 2024 according to World Development Indicators (WDI).

In 2016, 2017, and 2020, the population growth rate rose above the GDP growth rate. A 10-year view shows it is obvious there has been a decline in GDP per capita over the years, and this is not a good sign because it indicates that people are getting poorer on average.

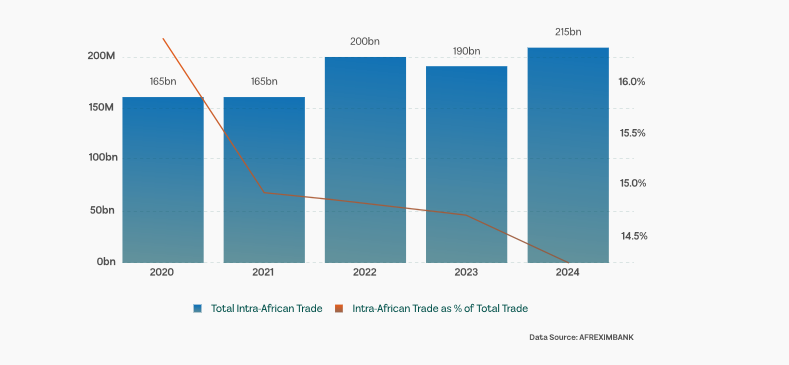

Recent global developments have intensified both the risks and opportunities confronting African economies. Climate change has heightened food insecurity and exposed weaknesses in energy and water systems. Tight global financial conditions and elevated inflation have increased pressure on public finances and reduced fiscal space. Simultaneously, technological advances are particularly in digital finance and mobile connectivity, creating a new pathway for inclusion, domestic capital mobilization, and service delivery. The launch of the African Continental Free Trade Area (AfCFTA) further underscores the potential for regional integration to reshape trade, industrialization, and market scale.

Against this backdrop, sector-specific gains in agriculture, finance, or energy have often failed to deliver lasting impact because progress in one area has been undermined by constraints in others. Sustainable growth in Africa depends on the effective alignment of multiple systems: food and land use, financial intermediation, energy and infrastructure, labour markets, technology, and governance. The Africa Grow report is developed in response to this complexity. It adopts an integrated, data-driven framework that examines six interdependent pillars—Agriculture and Food Systems; Banking, Investment and Capital; Environmental, Social and Governance (ESG); Fintech and Innovation; Jobs, Economy and Trade; and Power, Infrastructure and Energy. Together, these pillars represent the foundational systems through which economic growth is generated, financed, distributed, and sustained.

By analysing performance across regions and countries, the report identifies both accelerators of growth and binding constraints that continue to limit Africa’s development potential. It places particular emphasis on the quality of growth—its ability to generate employment, improve resilience, attract long-term capital, and support social and environmental outcomes—rather than growth rates alone. Ultimately, the Africa Grow report seeks to inform a more strategic and coordinated approach to Africa’s economic transformation. It provides policymakers, investors, development partners, and private-sector actors with a shared analytical basis to prioritize reforms, deploy capital effectively, and shift the growth narrative from potential to performance.

Snapshot assessment of the six pillars (progress, gaps, and risks)

- Agriculture and Food Systems (AFS)

Agriculture remains the economic backbone of Africa, employing a large share of the workforce and contributing close to one-fifth of GDP on average, with even higher shares in East, Central, and West Africa. The report finds:

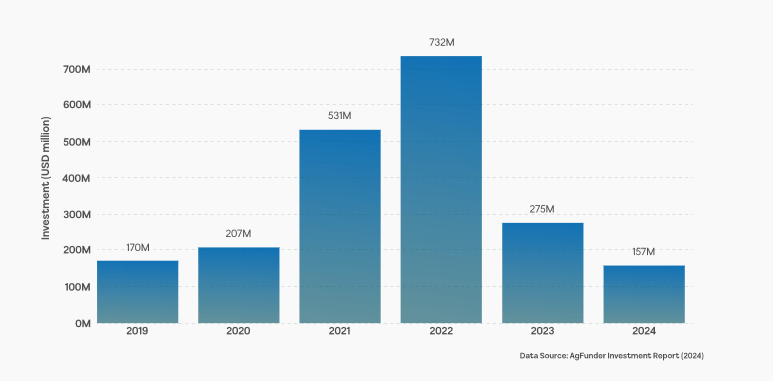

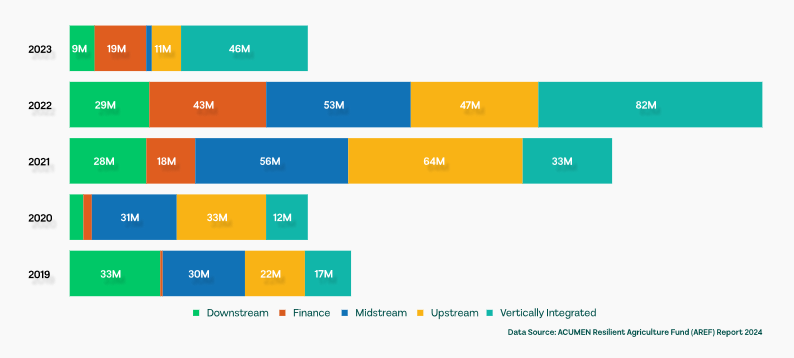

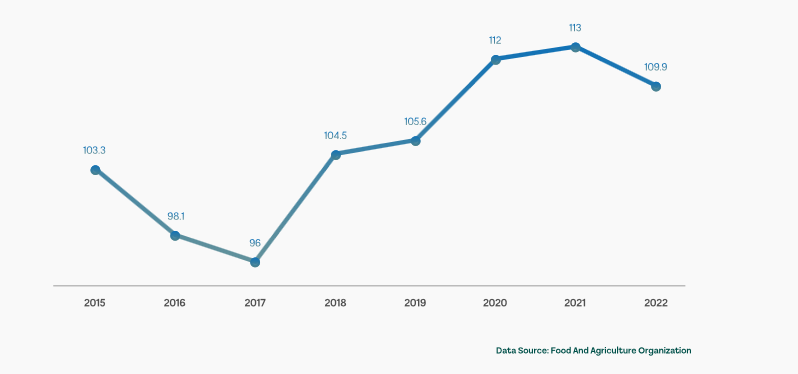

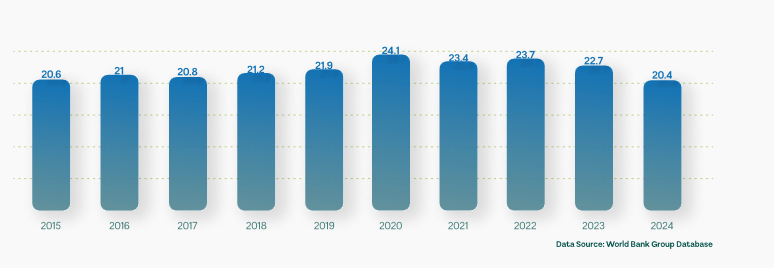

Rising investment momentum: Private investment in agri-food systems increased sharply after 2020, signalling a shift from subsistence farming toward commercial, technology-enabled agriculture. Public underinvestment: Government spending on agriculture has declined to around 2–3% of national budgets, far below the 10% target. Productivity gains but uneven outcomes: Food production indices have improved in several regions despite declining agricultural employment, indicating rising efficiency, but not sufficient to offset food insecurity.

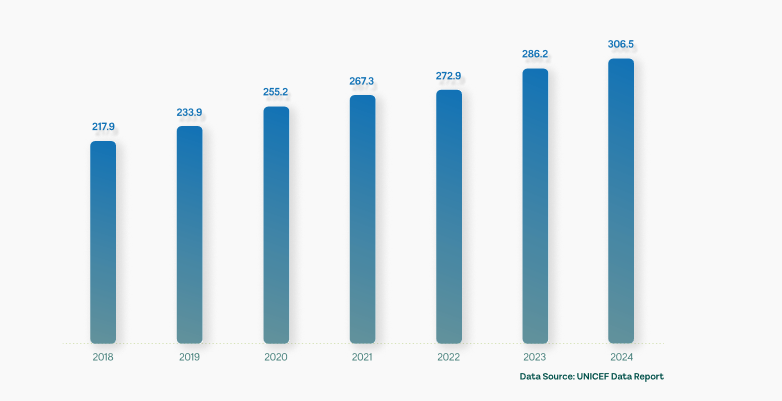

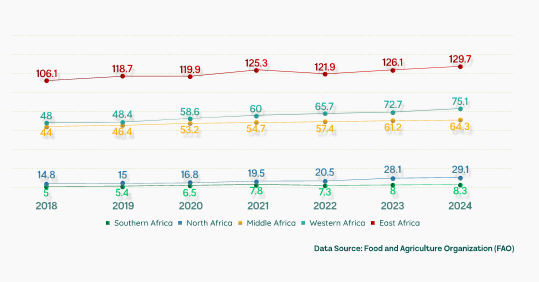

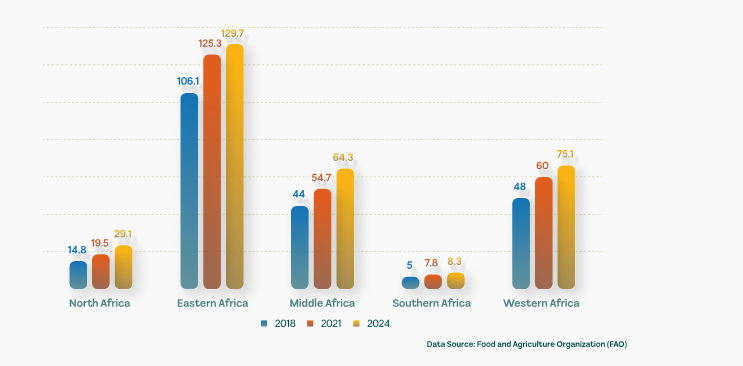

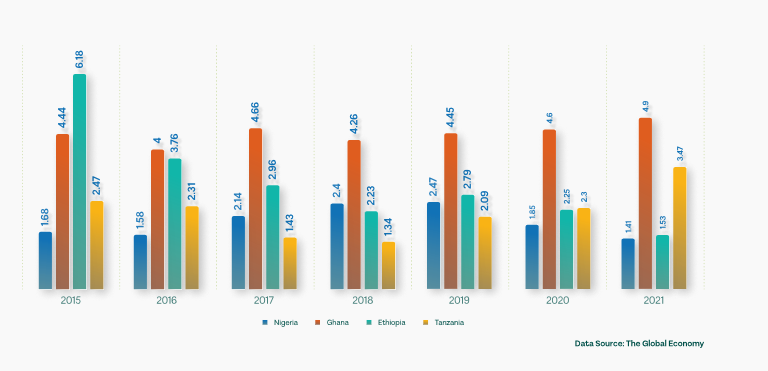

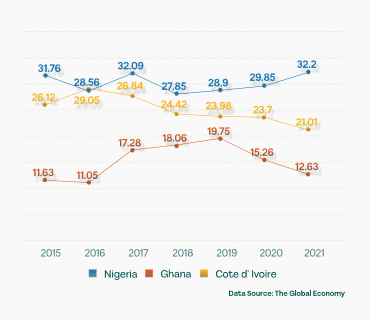

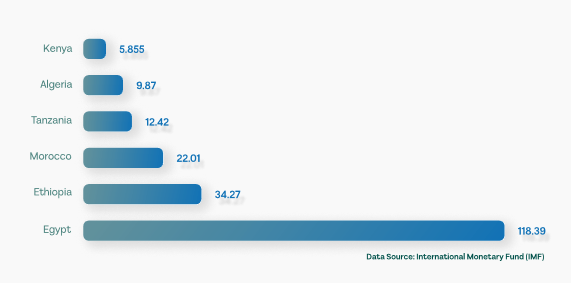

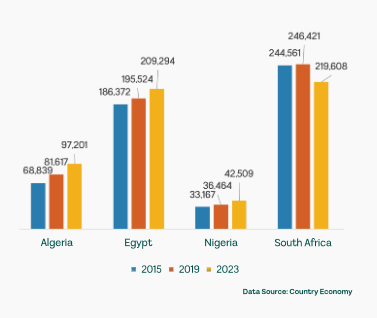

Deepening food insecurity: The number of undernourished people in Africa rose dramatically between 2018 and 2024, driven by conflict, climate shocks, inflation, and supply-chain weaknesses. The core insight is that productivity improvements alone are not enough. Without fertilizer access access, irrigation, storage, processing, and regional trade integration, rising output does not translate into affordability or nutrition security. - Banking, Investment, and Capital (BIC)

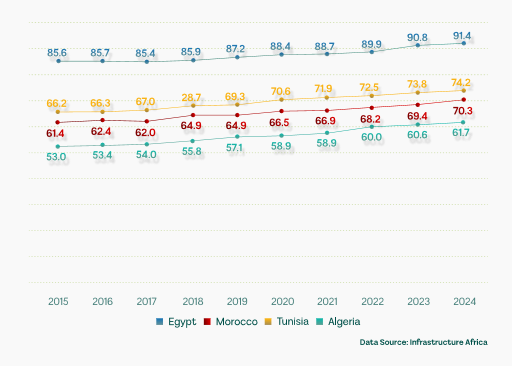

Africa’s financial system shows cautious resilience: Bank profitability is improving in several regions, supported by digitalization and cost efficiencies, particularly in East and West Africa. Foreign Direct Investment is recovering but remains below pre-pandemic peaks and is increasingly concentrated in energy transition, infrastructure, logistics, and digital sectors. Non-performing loans are trending downward in countries with stronger regulation and digital credit analytics, though they remain elevated in commodity-

dependent and fragile states. Inflation and currency volatility, especially in parts of West Africa, continue to undermine real returns and long-term investment confidence.

The report concludes that domestic banking systems are becoming the most reliable source of capital formation, especially in a world of unpredictable global capital flows. However, regional discrepancy risks widening inequalities unless macroeconomic stability and regulatory quality improve. - Environmental, Social, and Governance (ESG)

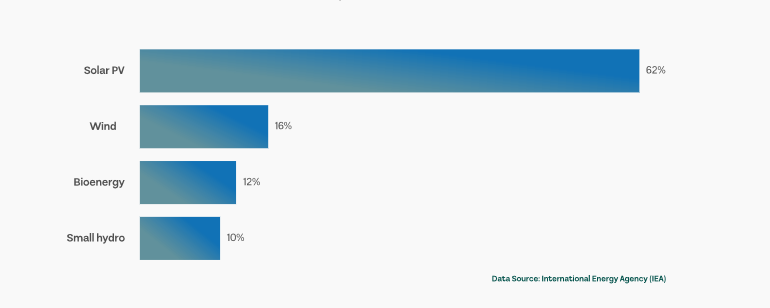

ESG is no longer marginal; it is increasingly shaping capital flows and policy choices: Climate vulnerability is rising, particularly for agriculture-dependent and low-income populations. African governments and banks are beginning to adopt ESG disclosure and sustainability frameworks, driven by investor pressure and multidimensional institutions. Renewable energy adoption is expanding, though unevenly, with hydropower and solar leading in different regions. Social investments in health, education, and clean cooking are increasingly framed as economic productivity investments, not just welfare spending.

The report warns that without stronger governance, data, and disclosure capacity, ESG risks will become symbolic. Regions with weaker institutions face exclusion from growing pools of ESG-aligned capital. - Fintech, Innovation, and Technology (FIT)

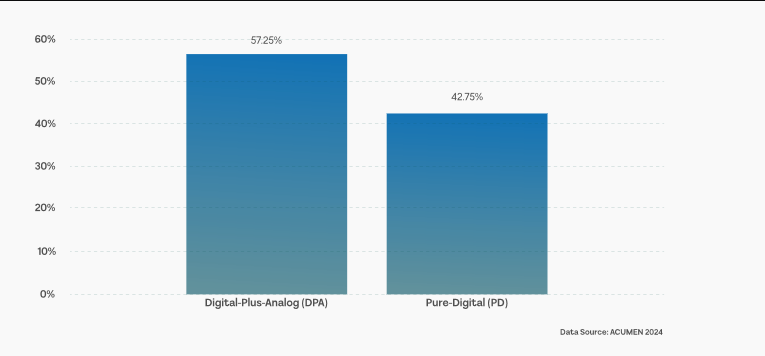

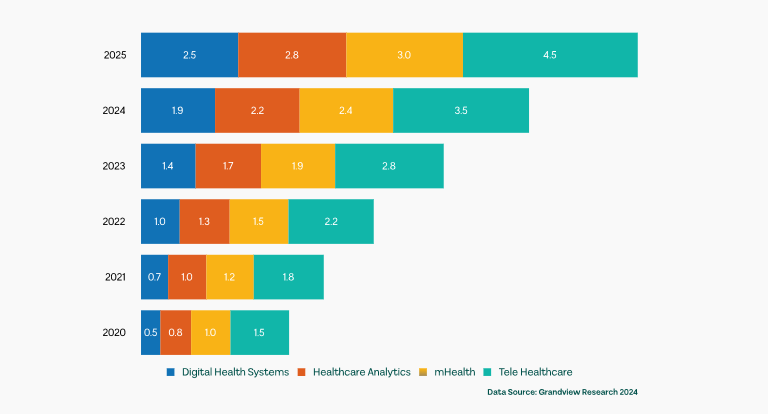

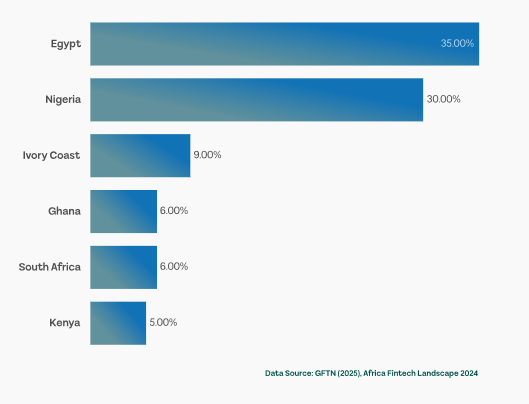

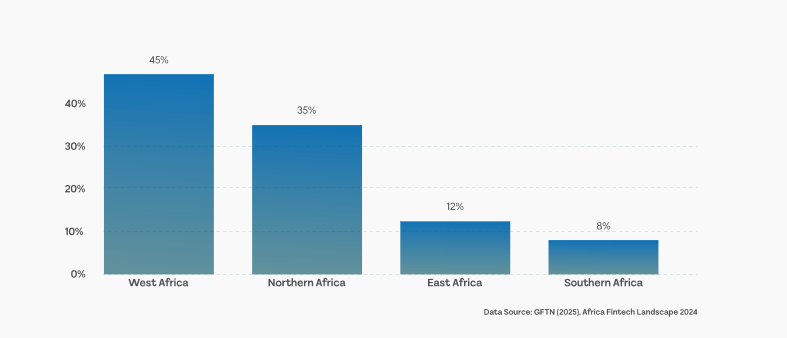

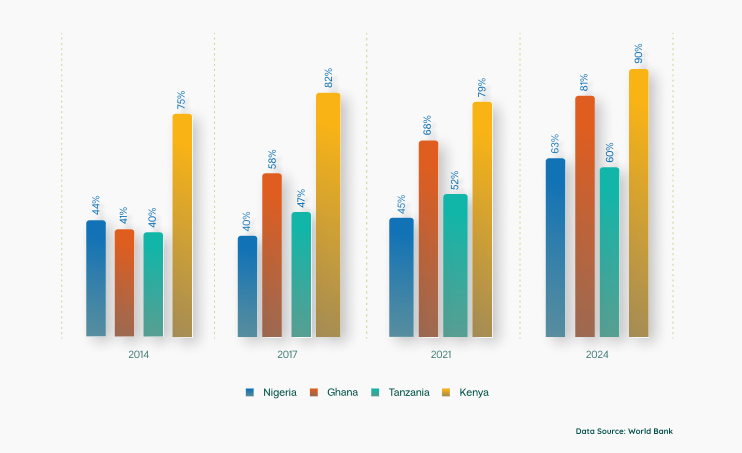

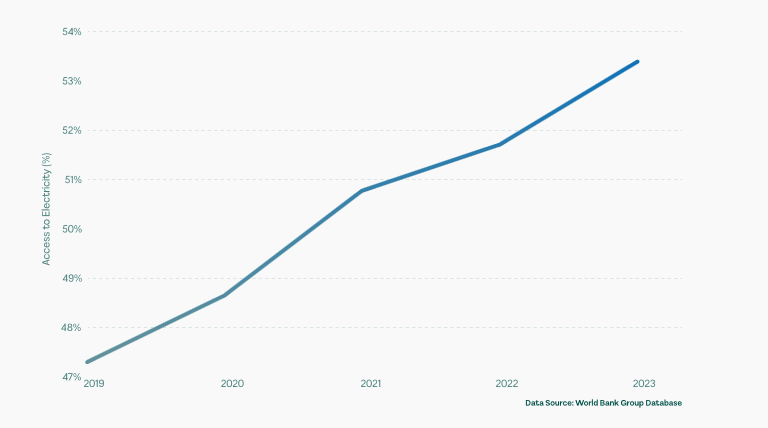

Africa is a global leader in mobile-money-led financial inclusion: Financial account ownership has risen rapidly, driven primarily by mobile money rather than traditional banking. Digital payments per adult have increased sharply, supporting formalization, SME activity, and household resilience. Fintech ecosystems have matured, with clear hubs in East and West Africa and growing spillovers into digital credit, savings, and micro-insurance. Infrastructure gaps and regulatory capacity remain constraints in Central and parts of North Africa.

The report finds that fintech has moved from access to impact, but sustained productivity gains will depend on digital trust, consumer protection, and interoperable regional payment systems. - Jobs, Economy, and Trade (JET)

Employment is the central pressure point of Africa’s growth report: Africa adds millions of working-age people annually, yet job creation falls behind population growth. Energy costs and logistics historically constrained manufacturing and trade, but the African Continental Free Trade Area (AfCFTA) is reshaping incentives for regional value chains and industrialization. Informality remains dominant, limiting productivity,tax capacity, and worker protection.

The report stresses that without structural transformation toward higher-productivity sectors, economic growth will continue to generate insufficient and insecure jobs, especially for youth. - Power, Infrastructure, and Energy (PIE)

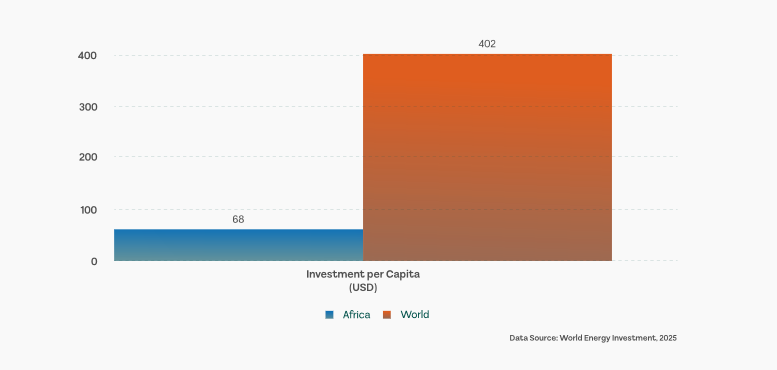

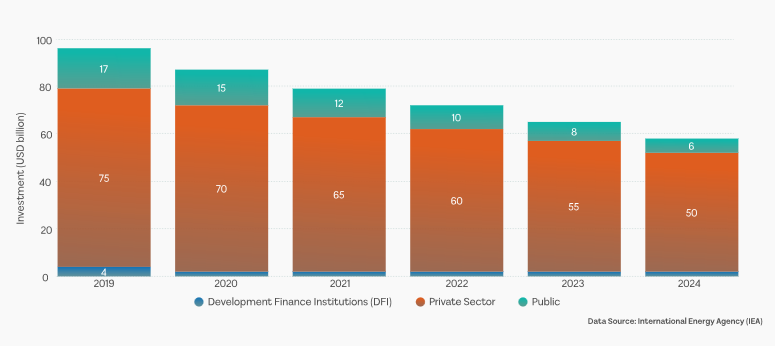

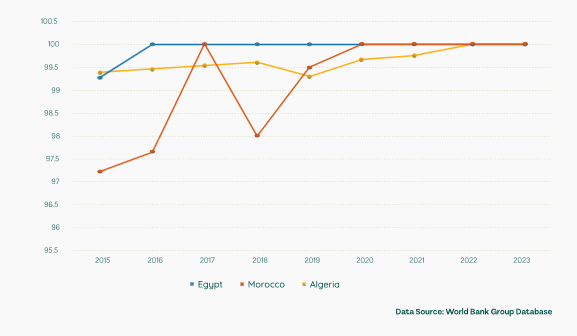

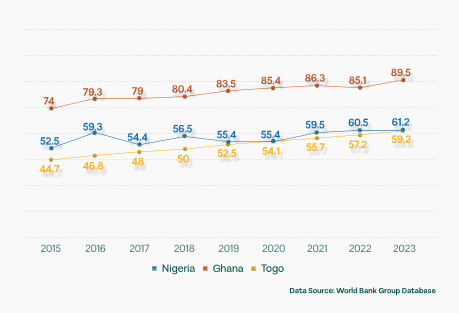

Energy and infrastructure are identified as binding constraints across all other pillars: Energy insufficiency continues to limit industrial growth, digital adoption, and service delivery. Renewable energy presents a major opportunity, supported by falling costs and new financing models. Infrastructure financing gaps remain large, but mixed finance and regional integration offer scalable solutions.

The key insight is that no pillar can succeed without reliable power and infrastructure, making this a foundational enabler of growth.

Key Cross-Pillar Strategic Insights

The report’s central contribution lies in showing how the six pillars interact as a system:

- Fintech amplifies banking efficiency and job creation

- Energy access determines the viability of agriculture processing, manufacturing, and digital services.

- ESG standards increasingly shape capital availability across all sectors.

- Weakness in power or governance pillars undermines progress in others.

How the six pillars jointly shape growth outcome

Agriculture and Food Systems remain the backbone of African economies, employing the majority of the workforce and contributing significantly to GDP. The Africa Grow pillar focuses on modernizing agricultural value chains, adopting climate-smart technologies, improving market access, and boosting productivity to achieve food sovereignty across the continent. Strengthening food systems is key to reducing poverty, promoting health, and ensuring long-term economic stability.

Banking, Investments, and Capital in Africa’s financial landscape are expanding, but access to capital remains uneven. This pillar aims to build robust banking systems, deepen capital markets, and unlock investment flows for businesses and infrastructure. Priority areas include financial inclusion, SME financing, investment-friendly regulatory environments, and innovative financing mechanisms capable of supporting large-scale development.

Environmental, Social, and Governance sustainability is no longer optional. This pillar emphasizes the integration of ESG principles into public policy, corporate strategy, and investment decision-making. By strengthening governance, promoting social inclusion, and adopting environmentally responsible practices

African institutions can improve resilience, attract global capital, and ensure that growth benefits people and planet.

Fintech, Innovation, and Technology in Africa are global frontrunners in mobile banking and an emerging hub for tech innovation. This pillar aims to connect digital transformation to expand financial access, improve service delivery, financial inclusion, and support entrepreneurship. It focuses on digital infrastructure, regulatory innovation, data governance, and the scaling of homegrown tech solutions.

Jobs, Economy, and Trade with the continent’s youth population set to double by 2050, job creation is a central development priority. This pillar emphasizes skills development, entrepreneurship, manufacturing, and expanded intra-African trade under the African Continental Free Trade Area (AfCFTA). Strengthening labour markets and productive sectors will ensure Africa’s economic growth is inclusive, self-motivated, and global-market ready.

Power, infrastructure, and energy in Africa are changing as reliable energy and modern infrastructure are essential for industrialization and digital growth. This pillar focuses on bridging Africa’s energy gap through renewable resources, expanding sustainable infrastructure, and improving logistics networks. Strategic investments in power, transport, water, and digital systems will support competitiveness and unlock vast economic potential.