Policy Architecture: The 2028 Horizon

Key Takeaway

This is a time-bound trade window, not a permanent regime. Investment strategies must account for a potential reversion after 2028.

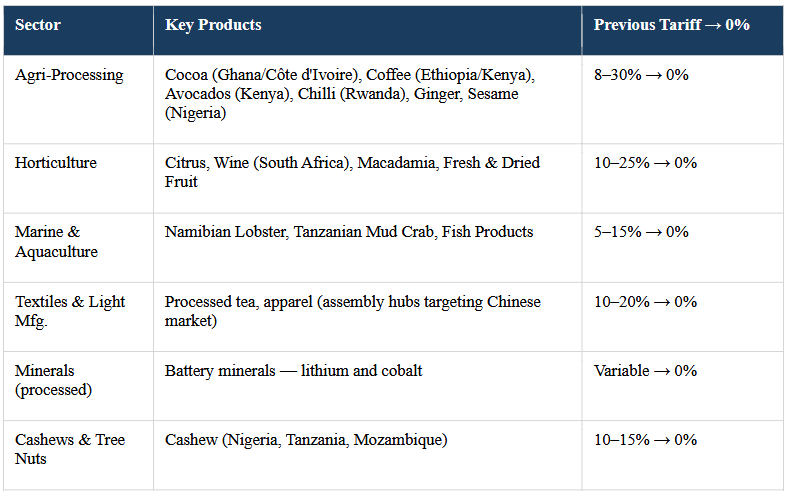

This initiative expands the 2024 framework for Least Developed Countries (LDCs) to major African economies including South Africa, Nigeria, and Egypt. Crucially, the rates are guaranteed only through April 2028, aligning with the broader 15th Five-Year Plan. This creates a deliberate sense of urgency for exporters to qualify and for investors to deploy capital. To support this, China has introduced “green channels” for agriculture and new direct shipping routes to compress logistics costs.