Growing Fast, Borrowing Faster: A Plain Look at Debt, Revenue, and the Tax Reform Test

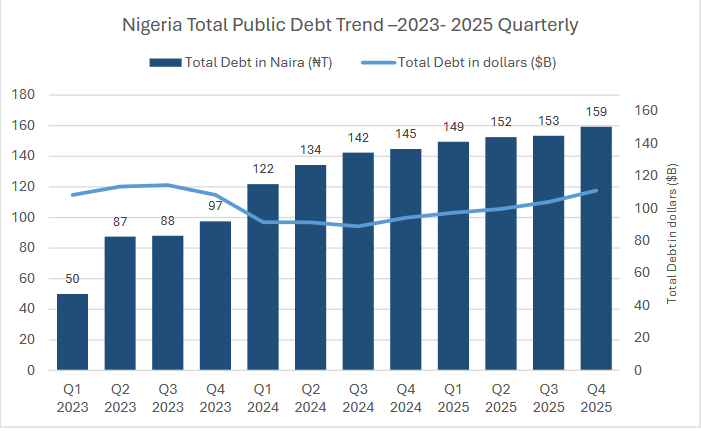

Figure 1 illustrates the quarterly trajectory of Nigeria’s public debt stock from Q1 2023 to Q4 2025,presented in both naira and US dollar terms. In naira, debt more than tripled from ₦49.85 trillion to ₦159.28 trillion. In dollar terms, however, debt fell from $108 billion in early 2023 to a low of $89 billion by mid-2024, before recovering to $111 billion by end-2025. The divergence reflects the naira devaluation of June 2023, which mechanically inflated the naira value of external obligations without representing new borrowing.

In response, the Nigeria Tax Act 2025 aims to strengthen non-oil revenue, simplify the tax system, and improve collection efficiency. However, the reform is still in its early stages, and uncertainty around implementation and revenue targets remains a key risk.

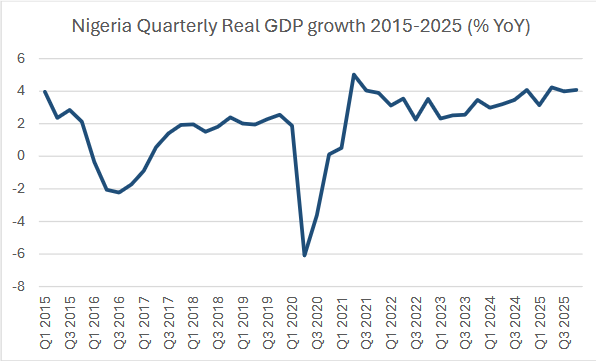

For investors, the picture is mixed: economic growth continues to support private-sector opportunities, while fiscal constraints are increasingly weighing on public spending–dependent sectors.

This brief explains how both growth and fiscal pressure can exist at the same time, what problem the new

tax law is designed to solve, and what this means for investors in Nigeria.